The European FinTech industry is shifting from a phase of rapid, capital-driven growth to one marked by consolidation, tighter regulation, and integrated business models. While the initial hype has faded, the sector continues to evolve through more deliberate strategic choices.

Since the 2021 funding peak, data from KPMG shows that FinTech investment deals in the EMEA region have dropped by 46% to 1,465 in 2024. Rather than signalling decline, the slowdown marks a phase of maturity that redirects firms toward sustainable growth and operational efficiency.

Europe’s challenge remains scale. According to data from BCG, in 2024, only around 8% of FinTechs generating over $500 million in revenue originated from Europe, compared to over 50% in the U.S. The fragmented market structure makes consolidation and integration essential for creating globally competitive players.

This article outlines the structure of the European FinTech ecosystem and examines three forces shaping its future: consolidation, regulation, and integration.

The Anatomy of the European FinTech Ecosystem

To comprehend the strategic shifts underway, it is essential to first understand the structure of the market itself. The European FinTech market consists of interdependent layers rather than a single, uniform industry. This structure provides the context for the competitive pressures and strategic opportunities that are currently defining the industry's trajectory.

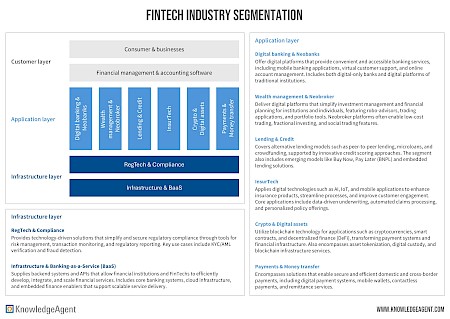

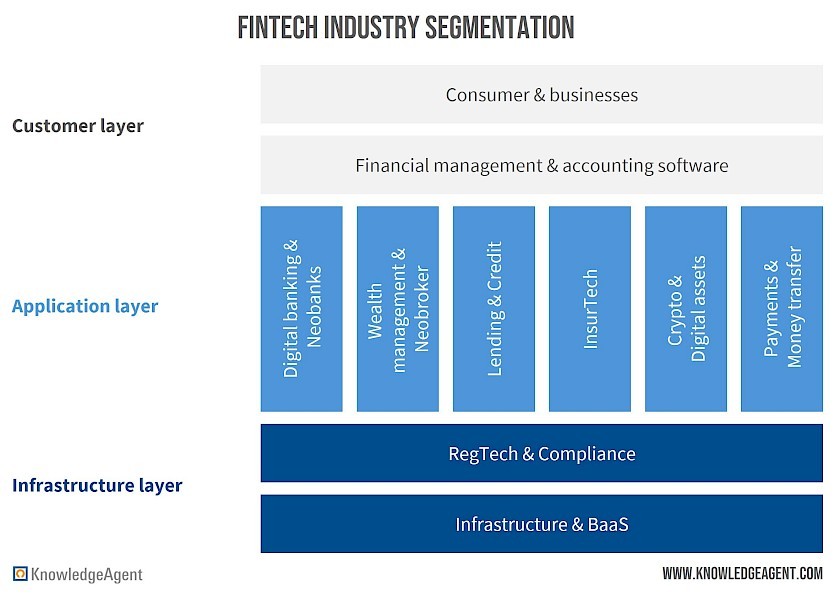

Figure 1: FinTech Industry Segmentation

The market can be conceptualized as a stack of three distinct but interconnected layers: the Infrastructure Layer, the Application Layer, and the Customer Layer.

The logic of this layered structure reveals a critical interdependence that has strategic implications. Innovation at the Application Layer, for example, a neobank introducing a new lending product, depends on the capabilities and compliance of Infrastructure partners. Regulations such as the Digital Operational Resilience Act (DORA) have increased the strategic relevance of RegTech and Banking-as-a-Service (BaaS) providers that ensure technical resilience and compliance.

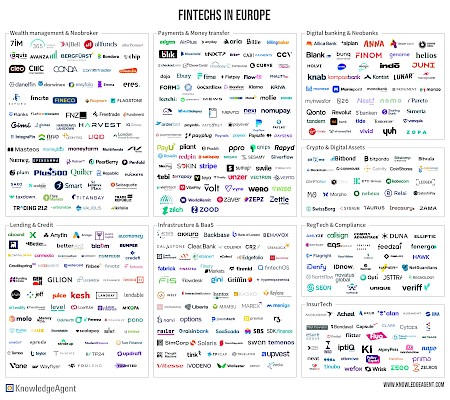

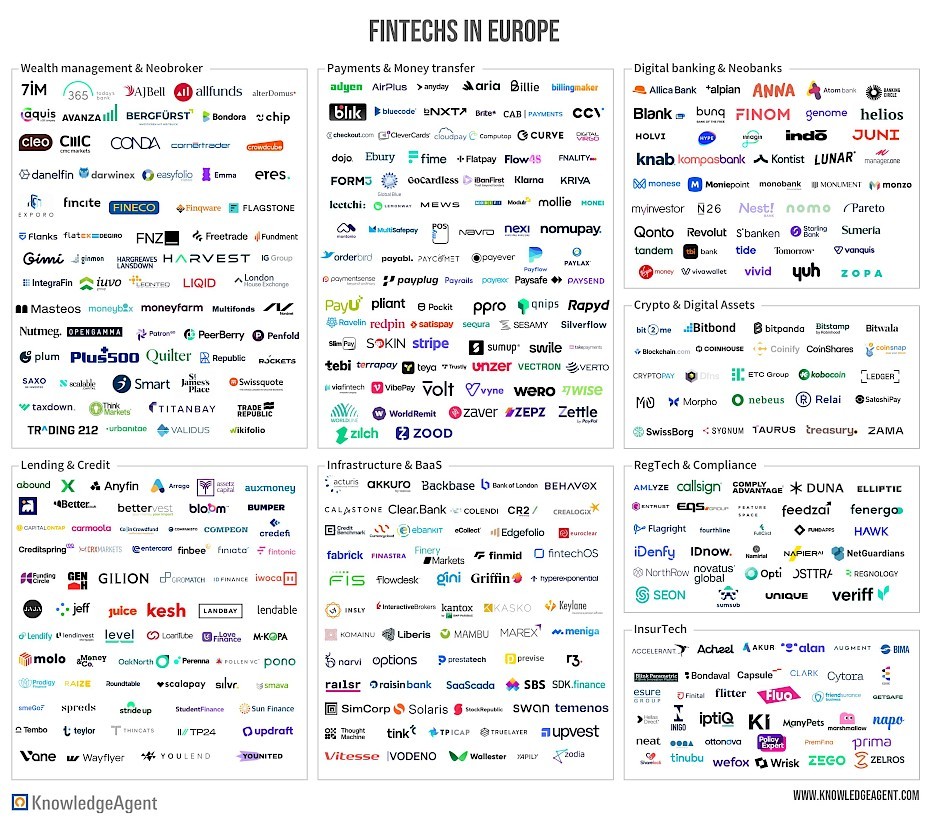

The accompanying market map shows areas where consolidation and integration are most active. The density of players in customer-facing Application Layer segments like Payments and Wealth Management signals a high potential for consolidation, while the companies in the Infrastructure Layer represent the strategic assets that enable the entire ecosystem's functionality and resilience.

Figure 2: Market Map: FinTechs in Europe

The Three Forces Reshaping European FinTech

With a clear understanding of the market's structure, the analysis can now turn to the three dominant forces that are compelling strategic change: consolidation driven by capital scarcity, restructuring compelled by regulation, and growth pursued through integration.

Market Consolidation Through M&A

Reduced venture funding has intensified competitive pressure, forcing a clearer distinction between winners and losers. As access to capital tightens, many smaller or less differentiated FinTechs are unable to sustain operations, leading to market exits.

At the same time, mergers and acquisitions have become a key path for growth and capability building. Larger incumbents and well-capitalized FinTechs are seizing the opportunity to acquire technologies, licenses, or customer bases from struggling peers at lower valuations. A notable example is UniCredit’s acquisition of Belgian lender Aion Bank and its BaaS partner Vodeno for €370 million, signalling that established banks increasingly prefer to buy rather than build technology. Mature BaaS platforms are becoming strategic assets, central to digital transformation efforts in traditional banking.

Regulations as a Market Maker

Simultaneously, a wave of EU-wide regulation is redefining the competitive landscape. Compliance demands are rising, but so are opportunities for firms able to adapt. Regulation now acts both as a barrier to entry and a growth driver for specialized RegTech providers.

An example of major changes in business practices resulting from new regulations is the ban of Payment for Order Flow (PFOF) that will fully take effect across Europe in 2026. In this practice brokerage firms receive payment from market makers in exchange for routing their clients' buy and sell orders to those market makers, resulting in a conflict of interest and cost inefficiencies for end consumers. While the ban is controversial, it is forcing a fundamental reinvention of the revenue models for many commission-free Neobrokers, such as Trade Republic, which have historically relied on this practice.

Further regulations reshaping the market:

- Markets in Crypto-Assets Regulation (MiCA): Uniform EU market rules for crypto-assets which were enforced in December 2024

- Digital Operational Resilience Act (DORA): Aims to strengthen the industry’s digital infrastructure and operational resilience against cyber threats. Came into force in January 2025

- Instant Payments Regulation (IPR): Requires all EU-based payment service providers (PSPs) within the eurozone to be able to receive instant payments. Since January 2025 all PSPs have to comply

The complexity of DORA, in particular, accelerates demand for “compliance-as-a-service.” Rather than building security and resilience internally, many FinTechs will rely on RegTech partners ‒ effectively turning regulation into a market-making force for the Infrastructure Layer.

Scaling Through Synergy

To overcome Europe’s fragmented market and tighter funding conditions, many FinTechs are scaling through integration. Only 21% of European FinTechs reportedly grew without partnerships. Integration follows three main paths:

- Partnerships: This is the most common and capital-efficient approach, involving collaboration with other entities to access new customers, technologies, or licensed capabilities. For instance, Digital asset platform Bitpanda partnered with Deutsche Bank to integrate real-time payments and provide German users with local IBANs. This gives Bitpanda enhanced functionality and credibility, while Deutsche Bank gains exposure to a younger, digital-native customer base.

- Vertical Integration: An alternative and capital-intensive vertical integration strategy involves a FinTech taking direct ownership of its core infrastructure, moving away from a reliance on Banking-as-a-Service (BaaS) partners. This approach provides greater control over the entire value chain, enhances efficiency, and accelerates the development of new products. A prime example of this is the German investment platform Scalable Capital. In late 2024, the company launched its own fully integrated platform and subsequently secured a full European Central Bank banking license in 2025. By bringing all critical functions in-house, the company is no longer dependent on third-party banking partners for core operations and new feature development.

- Horizontal Integration: This strategy focuses on expanding the range of financial services (within the application layer) offered to an existing customer base. The objective is to become a central, one-stop-shop for a user's financial needs, thereby increasing customer loyalty and lifetime value. Revolut exemplifies this approach. Having started with a multi-currency card, it has systematically expanded its offerings to include current accounts, stock and crypto trading, savings vaults, personal loans, and insurance products.

For any given FinTech, the choice between embedding its services into others' platforms or building its own all-encompassing platform is a critical strategic decision that will define its competitive landscape and long-term potential.

The Outlook for a Resilient and Strategic Market

European FinTech is entering a more disciplined phase. The post-boom environment favours firms that can combine financial prudence with strategic execution.

The market leaders of the next five years will be defined by their ability to master these new dynamics. Success will no longer be measured by user acquisition metrics alone, but by the capacity to:

- Execute targeted, capability-driven M&A to acquire critical technology and market position.

- Transform complex regulatory requirements from a compliance burden into a competitive advantage and a barrier to entry.

- Build and participate in deeply integrated ecosystems, whether through strategic partnerships, the vertical embedding of finance infrastructure, or the horizontal expansion of platforms to capture the full customer relationship.

While Europe may produce fewer unicorns than the U.S., its strength lies in building robust, interconnected, and compliant financial ecosystems. This trajectory points toward a more stable and strategically positioned FinTech market.

How KnowledgeAgent Can Assist

As a team, we are constantly monitoring markets and trends and have a deep understanding of market movements. We specialize in addressing your individual market and competitive intelligence needs. With our insights, you gain a solid foundation for confident, forward-looking decision-making.

Click here to contact our team!

Sources